Why many sustainability claims collapse in due diligence

Sustainability looks strong in strategy documents, but often looks weaker in due diligence. When organisations enter M&A, refinancing, or insurance review, the questions change. Ambition is no longer enough. Targets are not enough. Even certifications are not enough.

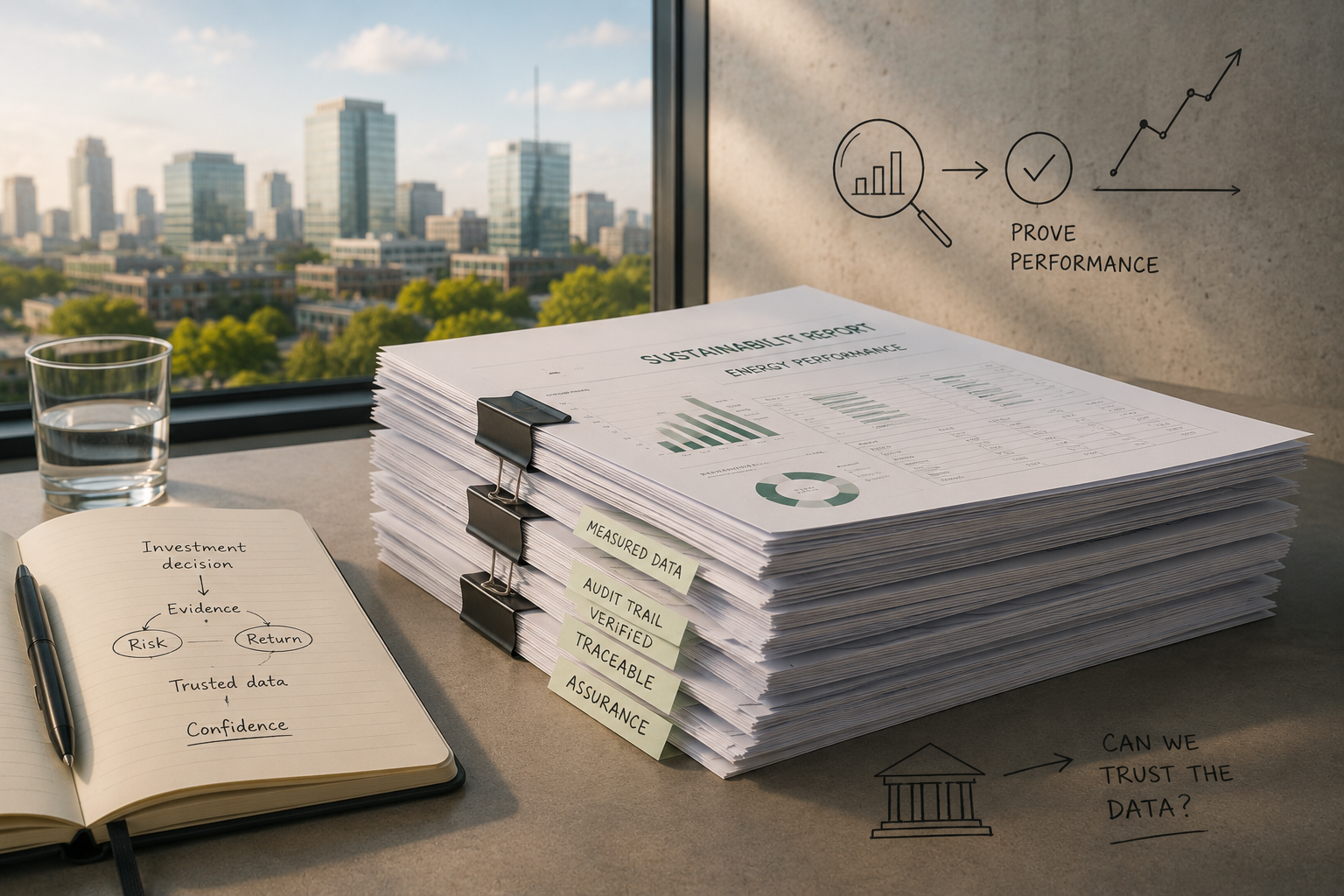

The focus shifts to evidence. Can performance claims be proven? Can improvements be traced to measurable outcomes? Can future exposure be modelled with confidence?

The problem is defensibility

Across sectors, organisations have invested heavily in upgrades, electrification, and efficiency programmes. But when investors or lenders examine the underlying data, they often find assumptions based on fragmented data rather than proof.

Projected savings instead of measured reduction, modelled carbon instead of operational performance or stated improvement instead of decision-grade evidence.

In a transaction environment, that gap becomes financial risk. If energy demand patterns are unclear, cost exposure cannot reliably be forecasted. If peak load risk is unmanaged and emissions performance isn’t backed by evidence, infrastructure constraints and pricing increases may create risk.

Suddenly, sustainability is no longer a reputational asset, but becomes a negotiation point.

Sustainability only matters when it can be proven

Sustainability only strengthens valuation when it is measurable, explainable, and defensible. In today’s market, performance claims aren’t trusted before they are tested. Investors, lenders, and insurers want to see how outcomes were achieved, what is driving demand now, and what risks sit ahead.

The organisations that protect value are not the ones with the strongest narrative. They are the ones with the strongest evidence.

Confidence comes from clarity. And in a market shaped by tighter regulation, grid constraints, and capital discipline, clarity is what separates credible strategy from exposed risk.

Want investment? Be prepared to prove your energy performance

There was a time when sustainability reporting was largely about demonstrating good intentions. That time...

The most expensive energy project is the one you never needed

When people talk about expensive energy projects, they usually mean the ones that ran over...

Every organisation has financial accounting. Soon, every organisation will need energy accounting

No business would make a major investment based on incomplete financial information. Imagine running a...

Energy price volatility is now a financial risk

Energy prices don’t just fluctuate anymore, they move in ways that are hard to predict...